Taylor Wimpey, Barratts and Persimmon report gloomy results and cost control measures

Some of the UK’s largest housing developers have posted cautious market outlooks, as house prices continue to fall.

Barratt Developments went first, reporting on Wednesday that the first half of the financial year had seen a marked slowdown in the housing market.

Implementing a recruitment freeze and reducing land approvals, the UK’s largest developer reported a drop in net reservations per week per site, falling to 0.3 in the three months to Christmas from 0.7 in the same period the previous year.

In addition, the fall in demand has impacted the firm’s forward order book, down from 14,818 homes in December 2021 to 10,511 in December 2022.

Political and economic uncertainty impacted the first quarter; this was then compounded by rapid and significant changes in mortgage rates which reduced affordability, homebuyer confidence and reservation activity through the second quarter.

david thomas, chief executive, barratt developments

Persimmon published a trading update the next day, reporting that they were pausing starts on 30 sites due to deteriorating sales.

Private net sales fell to 0.3 per site per week in the last quarter of the year, down from 0.77 in the same period last year. The overall private net sales rate in 2022 was 0.69 per outlet per week.

New home completions in the year increased by 2% to 14,868 (2021: 14,551) – but the firm’s forward sold position fell from £1.6bn in 2021 to £1.0bn in 2022.

We expect land spend in 2023 to predominantly relate to the settlement of land creditors, and we will take a highly selective approach to any new land purchases, investing only where we see the very best opportunities.

dean finch, group chief executive, persimmon

Taylor Wimpey then issued a trading update on Friday, revealing a consultation on a series of proposed changes to overheads and operations which could generate savings of £20m.

The developer also revealed controls to implement tighter cost scrutiny and a reduction in land commitments as they react to changing market conditions.

Net reservation rates fell to 0.48 per site per week in the second half of the year, bringing the rate for the full year to 0.68 homes per site per week (2021: 0.91).

Pricing in the land market is yet to reflect the changing market environment and with a strong land position and high quality outlets, we will continue to operate on a highly selective basis.

jennie daly, chief executive officer, taylor wimpey

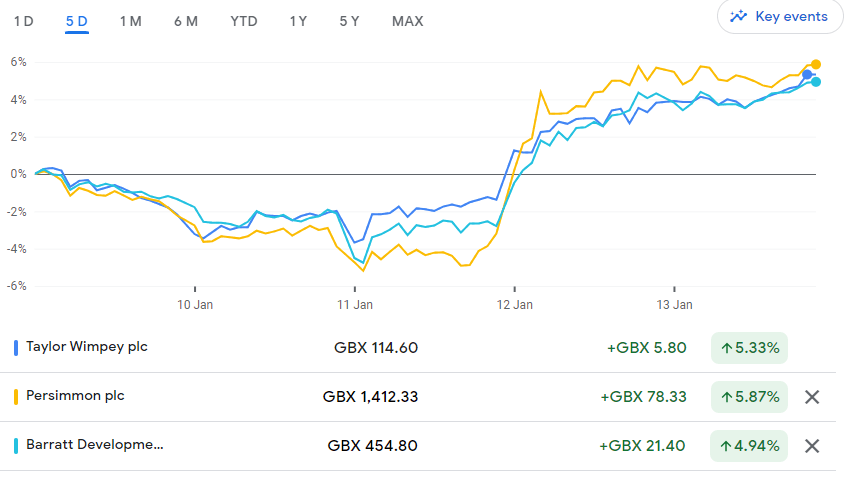

Despite the gloomy outlook for the year, share prices rose over the week as shareholders found confidence in each firm’s clear strategies and stable positions.

Bloor Homes, Britain’s largest privately owned housebuilder, reported a 21% increase in pre-tax profit in its accounts for the year to 30 June 2022, but warned that current economic conditions are creating a “mixed backdrop for the housing industry”.

It said: “Recent increases in the Bank of England base rate, and subsequent increases in mortgage loan rates, have made the landscape more challenging, but the company remains optimistic and well-placed to navigate the situation.”

Meanwhile, housing associations saw the number of homes built in 2022 increase by 22% – but with tighter margins.

The Regulator of Social Housing’s annual global accounts, which brings together financial data from over 200 associations, reports that 49,000 homes were built in the year to 31 March 2022; up from 40,000 in 2021.

However, overall operating margins fell to 20%, the lowest figure for 11 years.

House prices to fall 3.5% in 2023, as tender inflation stabilises

Ratings agency S&P Global has predicted that property values in the UK will fall by 3.5% in 2023 – the steepest drop in Western Europe after Portugal.

In an analysis of the European housing market, the firm stated that rising mortgage rates will impact house prices this year and next; but that prices would decline and not crash.

The report forecast a modest house price recovery of +2.7% in 2024.

Meanwhile, Experian have forecast a downturn of -2.4% in new work this year, driven by a -6.6% fall in new housing as house prices drop and the cost of living crisis continues.

In a construction forecast, the economics firm is forecasting a -1.7% dip in overall construction activity this year, before returning to modest growth in 2024.

However, Mace has announced a further downward revision of its tender price forecast for 2023, down to 2.5% from the previous forecast of 3.5%.

Reacting to an increase in construction output of 0.6% in Q3 2022, and a 6.4% increase in new orders, the consultancy firm reassessed its prediction.

Andy Beard, Global Head of Cost and Commercial Management for Consult, Mace, acknowledged a “difficult year ahead”.

He continues: “However, the construction industry’s moderate output growth and increase in new orders is an optimistic indicator for the industry to remain resilient compared with other sectors.

“The industry is likely to face obstacles in terms of material cost pressures and the impact of inflation on profit margins.”

Housing output falls in November, official figures show

Data from the Office for National Statistics (ONS) has revealed a fall in private housebuilding work of almost 5% in November, as developers responded to the fall in buyer demand after the mini-budget.

ONS figures showed that the private housing sector saw a £172m fall in output in the month to around £3.4bn, contributing to flat growth in the month for construction overall.

Public housing output also fell by 5.3% to £416m in the month, bringing the overall drop in housing output to 4.9%.