Latest market survey paints mixed picture

The February 2026 RICS Residential Market Survey has found that market momentum experienced earlier in the year has been tempered somewhat by “heightened geopolitical and macroeconomic uncertainty following the escalation of the conflict in the Middle East”.

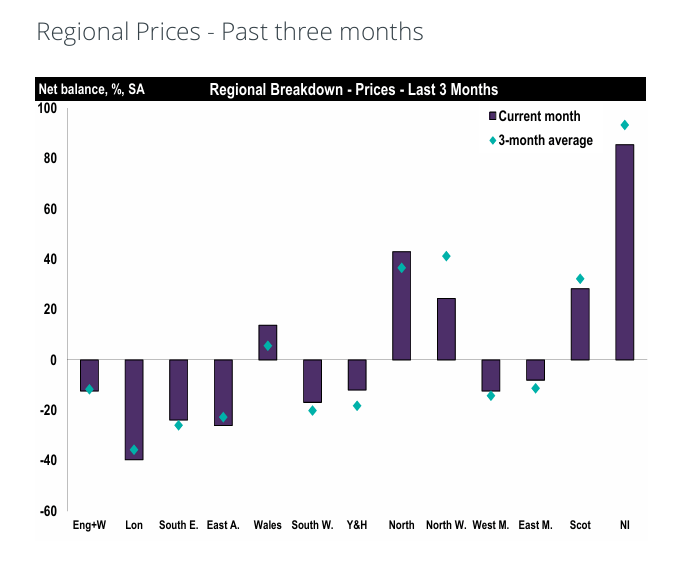

Buyer demand has weakened, with new buyer enquiries falling to a net balance of -26%, whilst agreed sales also remained negative at -12%.

House prices were described as broadly flat to slightly negative nationally, with the headline balance at -12%. However, the twelve-month outlook stayed positive overall, at 17%.

Meanwhile, a BCIS survey has found that housing developers are experiencing a 2% year-on-year increase in build costs in the fourth quarter of 2025.

The Building Cost Information Service’s Private Housing Construction Price Index sought responses from a range of small, medium and national builders, and found that 38% of respondents reported material costs to be the key inflation driver.

However, total construction output is estimated to have grown by 0.2% in January 2026, following three consecutive monthly falls in the last quarter of 2025.

Data from the Office for National Statistics found that an increase in repair and maintenance drove the improvement; but construction output from private new housing fell by -6.3% over the three months to January 2026.

HBF calls on government skills support

The Home Builders Federation held a parliamentary reception this week, in which they called on the government to “fully close” the construction skills gap.

The housebuilding body noted that the construction industry supported around 750,000 jobs in 2025 across a range of roles from design and architecture to construction and sales.

Neil Jefferson, HBF’s Chief Executive, said: “We’re proud of the positive impact industry initiatives are already having in attracting new recruits, upskilling our existing workforce and bridging the gap from classroom to site, but more must be done.

“With greater government support to expand opportunities and address constraints in the education system, we can build a resilient workforce capable of addressing the nation’s housing needs. Meanwhile, policy certainty and practical support for smaller builders – including demand-side measures and faster planning approvals – will enable industry’s employers to invest confidently in workforce development.”

Meanwhile, public engagement specialist Shared Voice called for planning consultation reform, describing the current system as “structurally flawed and risks undermining the delivery of homes and infrastructure”.

The firm has called for reform of the community consultation system, which it says tends to favour local opposition.

Developer and supply chain updates

Persimmon reported a strong 2025, with revenue up 17% to £3.75bn and completions rising 12% to 11,905 homes. Underlying pre-tax profit increased 13% to £445.6m, while underlying operating profit climbed 17% to £472.1m and margin edged up from 14.1% to 14.3%, helped by vertical integration and operational efficiencies.

Persimmon said it expects to deliver between 12,000 and 12,500 homes in 2026, but flagged potential risks from the conflict with Iran, including any impact on customer sentiment, build cost inflation and interest rates. The private average selling price rose 5% to £301,392, supported by a higher share of Charles Church deliveries and stronger conditions in some regional markets.

–

Berkeley Group has reaffirmed its pre-tax profit guidance of £450m for its current financial year, while warning that the emerging conflict in the Middle East could weigh on market sentiment. In its trading update for the period from November 1 2025 to February 28 2026, the group also said it expects 2027 pre-tax profit to be similar to 2026.

–

Forterra said it is protected against short-term gas market volatility, with around 80% of its gas usage for the rest of 2026 already secured and March fully covered. The company added that it has layered energy cover beyond that, with around 70% secured for 2027 and coverage extending, at reducing levels, through to 2030, helping shield it from price swings linked to the war with Iran.

Forterra also said that efforts to push through brick price increases last year were resisted by the market, suggesting demand conditions remain challenging. The update indicates a business focused on managing input cost risk while still facing pricing pressure on the sales side.

–

Builders’ merchants’ takings weakened in the fourth quarter of 2025, with the latest Builders Merchant Building Index showing like-for-like sales down -1.2% compared with Q4 2024. Volumes fell -2.9% while prices increased 1.8%, suggesting values were again being supported by inflation rather than underlying demand.

Compared with Q3 2025, the slowdown was sharper. Average daily takings dropped -9.0% and daily volumes fell -13.1%, while total takings were down -14.6% and volumes down -18.5% due to four fewer trading days in the quarter. Prices were 4.8% higher than in Q3.